Our niche is helping tradies (and their partners) find mortgages with lenders that accept pay through the Construction Industry Scheme.

There’s only a small group of lenders that do, and you should know because if you apply to the wrong lender, you could get rejected or be capped at borrowing a smaller figure based on your post-tax income.

You could borrow more with a lender that accepts CIS statements, as opposed to your tax returns.

A benefit of doing that is that both you and your employed partner, who is paid through PAYE (paid as you earn), can borrow based on pre-tax income (not what’s been earned after tax).

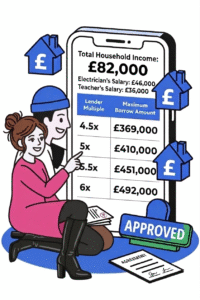

Hypothetically, let’s say you’re an electrician earning £200 a day. You work five days a week, resulting in a grand a week.

Some lenders will multiply your gross income by 46 (for 52 weeks in a year minus 6 weeks for presumed time taken off).

That would mean your income on the application would be £46,000.

Then there’s your partner’s income. Hypothetically, let’s say they earn £36,000 as a primary school teacher and are paid through the standard PAYE (pay as you earn) system.

Usually, though not always, CIS mortgage lenders will assess both incomes before tax, combine them, and then multiply them by 4.5 to 6 times. That’s how they calculate how much you can borrow for your joint mortgage.