We help tradeswomen find affordable mortgage deals. We specialise in CIS mortgages, so we know where to find the best lender if you work in a trade and are paid through the CIS scheme.

Most self-employed subcontractors think they need to be employed or ‘on the books’ to get a mortgage, but that’s not true.

In fact, being a subcontractor paid through the Construction Industry Scheme could help you to borrow more.*

Because they’ll calculate the maximum amount you can borrow based on your gross income (that’s the amount you earn before tax is taken away).

Apply for a mortgage with the wrong lender, and you could be limited to how much you can borrow because they might base how much you can borrow on your sole-trader profit (your post-tax income).

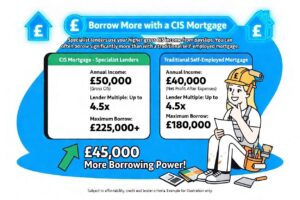

If your gross annual CIS income is £50,000, many lenders may allow you to borrow up to 4.5 times that (which is £225,000 or more, subject to affordability).

However, a mortgage lender that assesses net profit (and not gross income) could calculate a maximum mortgage of just £180,000 (assuming your net profit is £40,000).

That’s a potential £45,000 difference, which would impact your budget and therefore your choice of property.

That includes painters, electricians, plumbers, carpenters, site managers and masons who build, install systems, and finish interiors.

We know the subby-friendly mortgage lenders that accept income paid through the CIS scheme.

You are likely to be paid through the Construction Industry Scheme (CIS) if a contractor deducts 20% of your pay in advance for HMRC.

Another way to check whether you’re paid through CIS is to check if you’ve received a payment and deduction statement (or “CIS voucher”). You should receive one within 14 days of the end of each tax month, usually via email, post or by hand on site.

These statements provide essential legal proof of tax deductions, which are used for your self-assessment tax returns.

Women in UK trades are more likely than men to take time off or work part-time due to caring responsibilities, with over 1.46 million women out of the labour market for this reason.

Women are seven times more likely than men to leave work for family care, and twice as likely to take time off for stress or health issues.

Whether you’ve not been able to work because of illness, mental health issues, maternity leave or because you’ve been caring for children or family, we want to help.

The good news is that there is a selection of lenders that will accept 3 months’ of CIS statements as proof of income, so if you’ve been a subcontractor for less than a year or have gaps in your income, we want to find you a solution.

You don’t need 2 or 3 years of accounts to get a mortgage as a subcontractor, so get in touch with us today to learn more about your options.

As a woman working in a trade and paid via the Construction Industry Scheme, you have every right to a mortgage that reflects your true earning power.

Don’t let standard self-employed rules hold you back — with the right CIS mortgage, you can borrow what you need to buy a property you love and move forward with confidence.

Whether you’re a female electrician, plumber, gas engineer, carpenter, or painter, Opportunity Mortgages is here to help you find the best deal from lenders who understand how subcontractors are paid.

Fill out the contact form below or email alex@opportunitymortgages.co.uk for expert CIS mortgage advice.

We’ll match you with subby-friendly options and guide you every step of the way.